Social Security Has Been Boosted, Not Looted

By James D. Agresti

June 19, 2018

The newly released Social Security Trustees Report describes serious fiscal issues with the program and stresses that it should be reformed soon, or the situation will become much worse. However, public support for reform is impeded by a common fiction that inflames debate and distracts from the roots of the problem.

What the Report Says

The June 2018 Social Security Trustees Report states that “under the Trustees’ intermediate assumptions,” the program’s “total cost is projected to exceed its total income in 2018,” and trust fund reserves” will be “depleted in 2034.”

Moreover, the report details that Social Security’s long-term “actuarial deficit” is of such “magnitude” that fixing it with an across-the-board benefit cut would require “an immediate and permanent” 17% reduction in benefits for “all current and future beneficiaries.” Alternatively, fixing it with an across-the-board payroll tax increase would require “an immediate and permanent” 22% rise in payroll taxes.

As in previous reports, the trustees emphasize that “necessary changes” to keep the program “fully solvent” should be enacted “sooner rather than later” so that “more generations” share the burden of these changes and so they can be phased in “gradually and give workers and beneficiaries time to adjust to them.” Procrastination will only worsen these burdens, and “much larger changes would be necessary if action is deferred,” explain the trustees.

Roots of the Problem

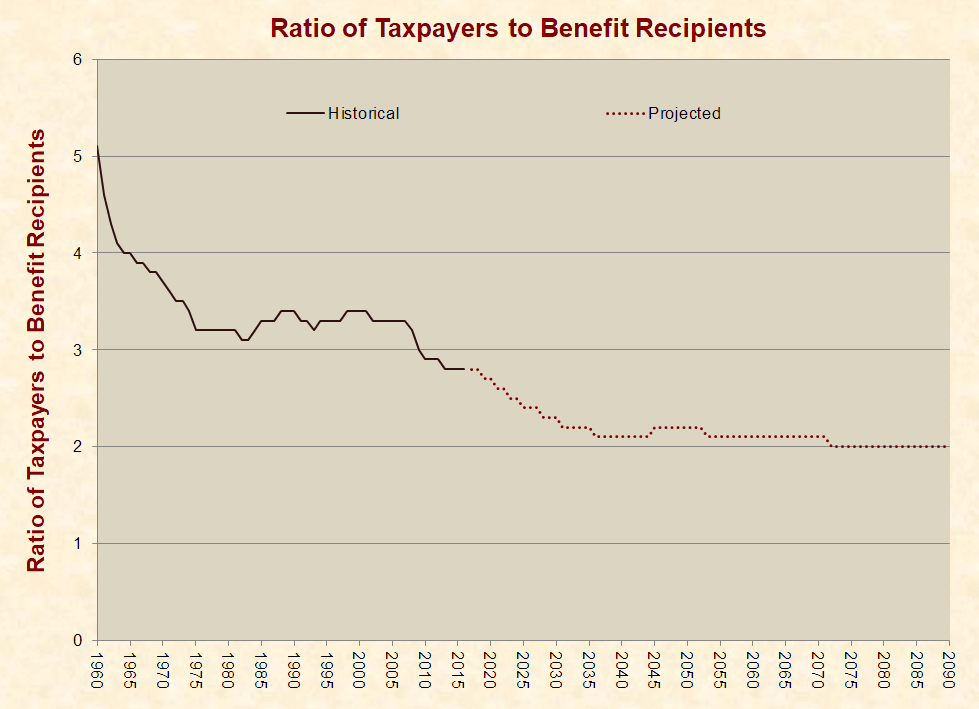

The primary cause of Social Security’s financial woes is that increasingly more people are receiving benefits from the program, while relatively fewer are paying into it. In 1960, 5.1 people worked and paid Social Security payroll taxes for every person who received benefits. This ratio has since declined to 2.8 to 1, and under the program’s intermediate projections, it will drop to 2.1 to 1 over the next 20 years:

Three major factors contributing to the falling ratio of taxpayers to benefit recipients are:

Three major factors contributing to the falling ratio of taxpayers to benefit recipients are:

- increases in life expectancy without comparable increases in the retirement age. Since Social Security began paying benefits in 1940, the average time spent collecting old-age benefits has increased by 45% for males and 47% for females.

- the higher birth rate of the baby boom generation compared to other generations. In two decades from the time that the first wave of baby boomers turned 65 years old in 2011, the number of people eligible for old-age benefits will increase by about 65%, while the number of people paying Social Security taxes will increase by about 18%.

- the rising number of people receiving disability benefits. Between 1965 and 2016, the U.S. population grew by 61%, while the number of people receiving disability benefits increased by 510%.

Despite these clear and dramatic changes that have undermined Social Security’s finances, the vast majority of voters blame the program’s problems on an imaginary cause.

Social Security Has Not Been Looted

In 2017, Just Facts commissioned a professional polling firm to conduct a scientific, nationwide poll of people who vote “every time there is an opportunity” or in “most” elections. While polls typically measure public opinion, this unique poll measured voters’ knowledge of public policy issues that affect their lives in tangible ways.

Among the poll’s 24 questions was this one: “Do you think Social Security’s financial problems stem from politicians looting the program and spending the money on other programs?” In total, 80% of voters replied “Yes,” including 78% of Democrats, 83% of Republicans, and 80% of third-party voters.

Yet, concrete facts prove the correct answer is “No.” In the words of Social Security’s trustees, federal law “prohibits expenditures from” the Social Security Trust Fund “for any purpose not related to the payment of benefits or administrative costs” of the program. Hard numbers confirm this to be true. Social Security’s actuarial records show that the program’s assets have increased or decreased by the difference between its receipts and expenditures in every year since its origin in 1937.

What some call “looting” is actually a legal requirement (established in the original Social Security Act of 1935) that all of the program’s surpluses be loaned to the federal government. Federal law compels the government to pay back this money with interest, and it has done this throughout the program’s history. In fact, since 2010, Social Security has been using interest received from the federal government to cover the shortfall between its expenses and non-interest income.

A common myth is that Democratic President Lyndon B. Johnson began using Social Security to finance other government programs in the late 1960s, but as documented by the Social Security Historian’s Office, “the financing procedures involving the Social Security program have not changed in any fundamental way since they were established in the original Social Security Act of 1935 and amended in 1939.”

Social Security Is Not a Savings Program

Feeding the false belief that Social Security has been looted is the assumption that the program saves workers’ money and later returns it to them. Thus, people suppose that any shortage of funds must be the result of looting.

However, Social Security is not structured as a savings plan, and it never has been. Instead, it mainly operates by taxing people who are currently working and giving this money to the aged and disabled. As explained by the National Academy of Social Insurance:

Social Security is largely a pay-as-you-go program. This means that today’s workers pay Social Security taxes into the program and money flows back out as monthly income to beneficiaries. As a pay-as-you-go system, Social Security differs from company pensions, which are “pre-funded.” In pre-funded retirement programs, the money is accumulated in advance so that it will be available to be paid out to today’s workers when they retire.

Likewise, the Social Security Administration states:

The money you pay in taxes is not held in a personal account for you to use when you get benefits. Your taxes are being used right now to pay people who now are getting benefits. Any unused money goes to the Social Security trust funds, not a personal account with your name on it.

Once again, hard data from the program confirms the statements above. From the start of Social Security in 1937 through the end of 2016, 94% of all Social Security payroll taxes were spent in the same year they were collected.

Even after accounting for all of Social Security’s income sources—including payroll taxes, taxes on Social Security benefits, transfers from the general fund of the U.S. Treasury, and interest earned by the Social Security Trust Fund—merely 13% of Social Security’s total income has accumulated in its trust fund during the program’s eight decades of existence.

Again, per the Social Security Administration:

Since the Social Security system has not accumulated assets equal to the liability of promised future benefits, the social security wealth that individuals hold represents a claim against the earnings of future generations rather than a claim against existing real assets.

After the federal government pays back with interest all of the money it has borrowed from Social Security, the program’s current claim against the earnings of future generations is $30.8 trillion. This amounts to an average of $132,914 for every person now receiving Social Security benefits or paying Social Security payroll taxes.

In sum, Social Security is not a savings plan but a government social program that provides benefits to the aged and disabled mainly by taxing people who are working. Some upshots of this reality are that certain people get nothing from Social Security after paying taxes for their entire working lives, while others receive far more from the program than they pay in taxes.

Certain legislators have sponsored bills to give Social Security an element of personal ownership like many other countries, but Congress has not taken any action on them.

Social Security Has Been Boosted

Contrary to the fable that politicians have taken money from Social Security, they have actually added money to it by:

- repeatedly increasing Social Security payroll tax rates and taxable maximums.

- leveling a tax on the Social Security benefits of individuals with incomes of more than $25,000/year and funneling these taxes back into the program.

- transferring money to Social Security from the general fund of the U.S. Treasury—which is funded by personal income taxes, corporate income taxes, excise taxes, estate and gift taxes, and other receipts.

To people who are under the illusion that Social Security has been robbed, the only fair course of action is to return the money. But since it hasn’t been robbed, adding money to the program will require more taxes. This has been the pattern of the past, and as a result, successive generations of Americans have gotten a progressively worse deal from Social Security.

For example, workers who earned average wages and retired at the age of 65 in 1980 recovered the value of their payroll taxes (including interest) after 2.8 years of receiving benefits. For workers who retired in 2003, it will take 17.4 years. For workers who will retire in 2020, it will take 21.6 years. This assumes Social Security will have enough money to pay scheduled benefits for this entire period, which it is not projected to have.

Many want to “fix” Social Security by leveling more taxes on high-income workers, but this has been done before. Adjusted for inflation, the maximum annual payroll tax per person is now 8.7 times higher than the federal government promised it would ever be when it enacted the program. And per a Congressional Budget Office report on Social Security, “over their lifetimes most high earners receive much less in benefits than they pay in taxes.”

Nonetheless, Social Security is still headed towards insolvency, and public support for genuine reform is thwarted by falsehoods about “looting” and “savings” that make generations of Americans feel entitled to more and more of the next generations’ earnings.

A lot of time is spent trying to suggest that the trust fund has not been stolen from because there are IOUs in there.

The Federal Government is insolvent (having far greater liabilities than assets). An IOU from an insolvent agency (or person) isn’t worth anything.

These bonds are non-negotiable meaning they can’t be sold when the money is needed. Taxes will need to be raised to pay back those bonds or the nation will need to go further into debt to pay them off.

If I have nothing in my bank account and write myself a million dollar check… am I suddenly a millionaire? No. Why? Because that check is simultaneously an asset and a liability. I’m still at $0. Those bonds are identical. They are both an asset and a liability… and are created by an insolvent entity.

80% of American knows the deal, the trust fund CASH has been taken and replaced with promises to steal from future generations.

You are completely missing the point. This article is about the finances of the Social Security program, which are legally separated from other operations of the U.S. Treasury.

Just Facts has covered the issue of the government’s ability to repay Social Security here. The federal government is in bad fiscal shape, but it is not insolvent, because it pays its debts and has the power to tax us.

But if it raised taxes to what it would take to avoid insolvency, we’d have another Boston Tea Party if not French Revolution.

“Taxes will need to be raised to pay back those bonds or the nation will need to go further into debt to pay them off.”

This is not correct. Since the money owed by the Treasury to the Social Security Trust Fund is part of the total national debt, issuing regular bonds in order to pay Social Security benefits will not increase the debt by one dime, since when money is paid back to the Trust Fund it reduces the amount owed to the Trust Fund. Net result: Increase in debt owed to other bond-holders, equal reduction in debt owed to Trust Fund, no increase or decrease in total national debt.

Eye opening and very informative. Still, by eliminating the cap on taxable income, Social Security would be on a more secure footing to pay full benefits.

Continuing to raise taxes to fund Social Security will eventually pit the youth against the elderly.

With only 2 workers for every one retiree now, the greatest Ponzi scheme in world history is starting to unravel. There is no way that young people can be taxed enough in future years to maintain this scheme without revolting. And a general fund that is already running $1 trillion deficits per year is not going to be able to bail it out. So get ready for the greatest Rip-Off ever – baby boomers who paid enormous sums into the scheme are now going to get their “benefits” slashed well below what we are being promised. And if we revolt, is an inter-generational civil war inevitable? All signs point to a future hyperinflation to write down the debts.

Just The Propaganda.

If Social Security was always meant to be a pay-as-you-go system, why was a “trust fund” set-up and why are we sent statements about how much our retirement benefits will be based on our annual earnings? Clearly these actions are designed to cause average citizens to believe the system operates like a pension fund or annuity. Because if the government told baby-boomers the truth that our “benefits” are dependent on 60% fewer future workers paying taxes into the system, we’d all realize we’re getting taken to the cleaners.

The trust fund was set up so that the program could accumulate some assets. Without it, the program would be unable to pay full benefits anytime revenues were insufficient. Furthermore, it would have no way to store surplus revenues.

The Social Security Administration sent statements about how much our retirement benefits will be based on our annual earnings so that people could plan for their retirement.

It’s worth noting that President George W. Bush made social security reform a major part of his platform nearly 20 years ago. But he was roundly critiqued and demagogued by the Democrats and the press and Congress refused to address the issue. So here we are. One side of the aisle recognizes the problem and is willing to fix it. The other side is not; they only want it as an issue to run on. The problem is in our hands. Who’re you going to vote for?

Start raising the age at which people can collect until it again stands at that age at which there is a 90% morbidity rate – in other words, when most reasonable people would have expected that they would have already died, and therefore not planed for it.

Raise it one year in each even year until we get there (75? 80?), then tie it to mortality tables.

You can always spot the young healthy office workers comments on the retirement age articles.

Or, perhaps, by doing away with this worthless social program and allowing folks to keep their money, either to invest or to blow it and be broke later, if willing to pay the consequences of the latter.

That’s the best path to follow… Some sort of pay off for those who are in the program followed by the ever so rational plan you propose… save or starve.

And what a scam the “trust fund” turned out to be! Sold as a fund to prepare for the days (now) when there would be 2 instead of 5 workers for every beneficiary (so taxes wouldn’t have to be raised on future works to untenable levels), it just provided the politicians a slush fund to spend away and leave us with the IOUs (and the need to still raise the taxes to untenable levels anyway to pay the IOUs). Shame on Ronald Reagan for foisting this scam on us all the while he opined about how crooked the “guvment” was.

You should read the article so that you are informed regarding your “such fund” comment.

So you think Reagan started SS in the 1980’s?

The US needs to do the same thing Greece has done to adapt to the new reality. Need to cut the benefits for those receiving them now by what is needed to keep it going as a pay as you go system. Period. Greece dug themselves out of a hole and is running surpluses now and they have a much weaker economy than the US. The Social Security System is needed since most employers do not provide retirement benefits and those programs are drying up as well. Time to get on with it and do what is needed by establishing an advertising campaign to stop the nonsensical fairy tales of how the government works. The older generation did the hard work and fought the wars so that we exist. Go ask those in war torn countries with a dysfunctional government if they would like to pay our taxes to live here. Every person who lives in real dire circumstances would jump at the chance to get into our system. We need to stop this populist lie about how bad the US Government is because for those of us who are veterans it is an insult to our wonderful country.

I wonder if the money the government borrowed from the SS funds is counted in our deficit number?

It is counted in the national debt but not in the deficit figures typically reported by the government and media: https://www.justfacts.com/nationaldebt.asp#government-deficits

OBVIOUSLY, OUR SO CALLED “WE THE PEOPLE REPRESENTATIVES” IN WASHINGTON ARE A WHOLE LOT MORE INTERESTED IN SERVING THEMSELVES, AND THEIR OWN INTERESTS, THAN THEY ARE IN DOING WHAT THEY ARE THERE TO DO, AND THAT IS TO: 1.) FOLLOW THE CONSTITUTION, 2.) ABIDE TOTALLY BY THEIR FORMALLY TAKEN OATH OF OFFICE, AND 3.) ACTUALLY AND HONESTLY REPRESENT “WE THE PEOPLE” IN EACH AND ALL OF THEIR DEALINGS. WHY HAS THAT BEEN SO DIFFICULT TO DO FOR OUR ELECTED AND APPOINTED OFFICIALS ?

What percentage rate is the Government paying back to the SS Fund. If it is less than the public market percentages, then the government is effectively stealing from us.

The three counties in Texas that opted out of Social Security could teach the Social Security Trustees, Congress, etc several things: https://www.forbes.com/sites/merrillmatthews/2011/05/12/how-three-texas-counties-created-personal-social-security-accounts-and-prospered/#24d021993283

Excellent question.

In 2016, the U.S. government paid an effective annual interest rate of 3.2% on the debt that it owed to Social Security: https://www.justfacts.com/socialsecurity.asp#impact-debt

In comparison, the government pays an average interest of about 2.1% on all of its publicly held debt. Just Facts will be publishing research on this topic soon.

Here is the promised research: https://www.justfacts.com/nationaldebt.asp#interest

Doesn’t S.S. Disability come out of the ‘General Fund’?

For workers, disability comes out of Social Security. However, the Supplemental Security Income (SSI) program provides benefits for aged, blind, and disabled people without regard to prior workforce participation. It is administered by the Social Security Administration, but it is not funded by Social Security taxes. https://www.justfacts.com/socialsecurity.asp#overview

If it is not a “personalized” account then why do I have a personal SSN and why do I get personal statements with projections of what I will receive, which from analyzing them do indeed seem to be based upon what I am putting in???

There is no real “trust fund.” It is just promises to pay back later what the government spent in the past. Been this way from the beginning. If any private person had set this up they would be in jail. It’s a fraud. It’s a Ponzi scheme.

While this analysis may be “factual” within your narrowly defined parameters, it ignores the non-GAAP nature of SS accounting. Assets such as “special issue securities” which can’t be sold (valued) on the open market have no GAAP value outside the “interest” the government supposedly pays the SS Trust Fund by first borrowing it from the public or the Federal Reserve and adding it to the current $21 TRILLION debt. The total of all taxes collected, including the SS “deduction”, has rarely been sufficient to cover total annual government spending. The fact the federal government can issue unlimited debt is the one and only reason SS can be considered solvent under any truthful financial argument. If you had simply included a caveat in your article indicating the non-GAAP nature of SS accounting, I think most readers would be okay with the contingent nature of your facts about SS – especially that part about SS being “boosted”. LOL

There is a statement I don’t understand: “Some upshots of this reality (social program) are that certain people get nothing from Social Security after paying taxes for their entire working lives, while others receive far more from the program than they pay in taxes.” What do you mean that they receive nothing? I thought that if workers paid for some quarters over the working careers that they would receive at least a pittance?

Simply follow the hyperlink in the statement. For convenience, here it is: https://www.justfacts.com/socialsecurity.asp#personal-heritability